Understanding Unison Equity Home Sharing Agreement and What Happens If the House Burns Down

Unison offers a unique financial product called the Unison Equity Home Sharing Agreement, which allows homeowners to access a portion of their home’s equity in exchange for a share in future appreciation or depreciation of the property. This arrangement can be appealing to homeowners looking for an alternative to traditional loans or home equity lines of credit (HELOCs). However, questions arise regarding what happens in extreme situations, such as if the house is damaged or completely destroyed by fire.

What Is the Unison Equity Home Sharing Agreement?

The Unison Equity Home Sharing Agreement is a financial partnership where Unison provides a lump sum of cash to a homeowner in exchange for a percentage of the future change in the home’s value. Unlike traditional loans, Unison does not charge interest or require monthly payments. Instead, when the homeowner sells the property or reaches the end of the agreement term (usually 30 years), Unison collects its agreed-upon share of the home’s appreciated (or depreciated) value.

This arrangement offers flexibility, particularly for homeowners who need access to funds but do not want to increase their monthly debt obligations. The funds can be used for various purposes, such as home improvements, paying off debts, or investing in other opportunities.

What Happens If the House Burns Down?

A major concern for homeowners considering a Unison agreement is what happens if the house sustains significant damage, such as from a fire. Unison structures its agreements with protections for both parties in such an event.

In the unfortunate event that your home, under a Unison Equity Home Sharing Agreement, is destroyed by a wildfire—such as the Palisades Fire in January 2025—the following considerations apply:

Insurance and Rebuilding:

- Homeowner’s Insurance: As a homeowner, you are typically required to maintain comprehensive homeowners insurance, which should cover damages from natural disasters like wildfires. In the event of destruction, the insurance payout is generally used to rebuild the property.

- Reconstruction Obligation: Unison’s agreements often stipulate that in the event of significant damage or destruction, the homeowner is obligated to use insurance proceeds to restore the property to its original condition. This ensures that the asset (the home) securing Unison’s investment is preserved.

Impact on Unison Agreement:

- Valuation Post-Reconstruction: Once the home is rebuilt, its value may be reassessed. The terms of the agreement regarding Unison’s share in the property’s appreciation or depreciation would continue based on this new valuation.

- Potential Buyout: If rebuilding is not feasible or if you choose not to rebuild, the agreement may require a buyout of Unison’s share. The buyout amount would typically be determined based on the property’s value prior to destruction, as outlined in your contract.

Steps to Take:

- Notify Unison: Inform Unison promptly about the damage to discuss the implications for your agreement and understand your obligations.

- File Insurance Claims: Initiate claims with your homeowners insurance to cover the loss and fund the rebuilding process.

- Review Agreement Terms: Carefully examine your Unison agreement to comprehend the specific terms related to property destruction and rebuilding obligations.

- Consult Professionals: Engage with legal and financial advisors to navigate the complexities of rebuilding, insurance claims, and fulfilling the terms of your equity sharing agreement.

It’s crucial to act swiftly and maintain open communication with all parties involved to ensure compliance with contractual obligations and to facilitate a smooth recovery process.

What If the House Is Not Rebuilt After Being Destroyed by Wildfire?

If the house is not rebuilt after being destroyed by a wildfire, such as the Palisades Fire in January 2025, the Unison Equity Home Sharing Agreement may be affected in the following ways:

Key Considerations:

- Insurance Payout and Unison’s Share

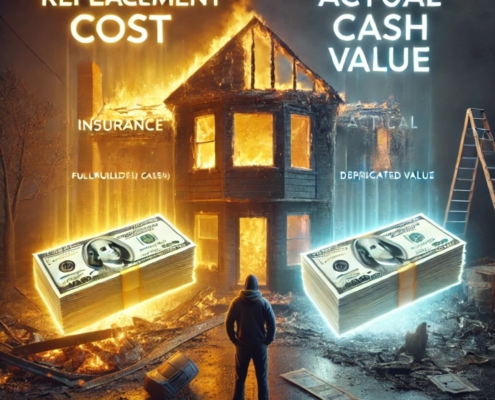

- If you do not rebuild, your homeowners insurance would likely issue a payout based on the replacement cost or actual cash value of the home.

- Unison may have a claim to a portion of the insurance payout, depending on the agreement terms.

- The insurance proceeds would generally be used to settle outstanding obligations, including Unison’s share.

- Agreement Termination and Buyout

- If the home is not rebuilt, the property no longer exists, and the Unison agreement would likely need to be settled.

- You may be required to buy out Unison using insurance proceeds or other funds.

- The buyout amount would be based on the home’s pre-disaster market value, as determined by an appraisal or other valuation methods outlined in the agreement.

- Land-Only Valuation

- If the structure is destroyed but you retain the land, the land value could be used to determine Unison’s equity share.

- If you sell the land, Unison would receive its share of the proceeds based on the agreement terms.

- Loan or Foreclosure Risks

- If the property was mortgaged, your lender may require that the insurance payout be used to pay off the loan first before any funds are distributed to you or Unison.

- If there are insufficient insurance funds to pay off both the mortgage and Unison, you may be responsible for covering the shortfall.

- If obligations are not met, it could lead to legal action or forced sale of the land.

What You Should Do:

- Review Your Unison Agreement – Check for specific clauses about property destruction and settlement obligations.

- Communicate with Unison – Discuss options, including potential buyout terms or land sale scenarios.

- Work with Your Insurance Provider – Understand the payout structure and whether it covers rebuilding, buyouts, or other obligations.

- Consider Legal & Financial Advice – A real estate attorney or financial advisor can help navigate negotiations with Unison and your lender.

If your home was completely destroyed in a wildfire, such as the Palisades Fire in January 2025, your exit options for the Unison Equity Home Sharing Agreement will depend on insurance coverage, Unison’s agreement terms, and financial feasibility. Here are the main exit strategies in such a scenario:

1. Use Insurance Proceeds to Settle the Agreement

If you have homeowner’s insurance with fire coverage, your insurance company will provide a payout based on:

- Replacement cost (to rebuild)

- Actual cash value (current market value, considering depreciation)

How it Works:

- If you do not rebuild, insurance proceeds can be used to buy out Unison’s share.

- The buyout amount will depend on:

- The pre-destruction appraised value of the home.

- How the agreement defines Unison’s share in a total loss situation.

✅ Pros:

- Fully settles the Unison agreement.

- No need to rebuild or take on new debt.

❌ Cons:

- If insurance does not fully cover Unison’s share, you may have to pay out-of-pocket.

- A total loss may complicate the valuation process.

2. Rebuild the Home and Maintain the Agreement

If you rebuild using insurance money, your Unison agreement may continue as normal.

How it Works:

- You use insurance funds to restore the home to its original condition.

- Unison retains its equity stake in the home’s future appreciation.

- Once rebuilt, you can later exit via sale, buyout, or refinance.

✅ Pros:

- Avoids immediate settlement costs.

- Keeps future appreciation potential.

❌ Cons:

- Rebuilding takes time and effort.

- Construction costs may exceed insurance payout.

- You remain locked into the agreement.

3. Sell the Land and Pay Unison’s Share

If the home is destroyed and not rebuilt, the land still retains value and can be sold.

How it Works:

- You sell the vacant land instead of rebuilding.

- The sale proceeds go toward:

- Paying off any existing mortgage.

- Buying out Unison’s share (if required).

- If the land’s value is less than Unison’s share, you may need additional funds.

✅ Pros:

- Easier and faster than rebuilding.

- Settles the agreement without requiring a lump-sum buyout.

❌ Cons:

- Land value may be significantly lower than the home’s pre-fire value.

- If Unison’s agreement is based on the pre-fire value, the land sale may not fully cover the buyout.

4. Negotiate a Settlement with Unison

If rebuilding is not an option and the insurance payout or land sale is insufficient, you may be able to negotiate a reduced buyout with Unison.

How it Works:

- Explain that the home was destroyed and rebuilding is not financially feasible.

- Request a lower buyout amount based on the reduced property value.

- Unison may agree to a discounted settlement rather than waiting for a future sale.

✅ Pros:

- Reduces the financial burden of a full buyout.

- Provides an alternative if other options are not feasible.

❌ Cons:

- Unison is not obligated to agree to a reduced amount.

- The process may take time and require legal/financial negotiation.

Final Considerations

- Check your homeowner’s insurance policy for coverage details.

- Review Unison’s agreement for terms related to total loss scenarios.

- Consult a real estate attorney before negotiating with Unison.

The Unison Equity Home Sharing Agreement offers a valuable alternative to traditional home financing, but it’s essential to understand all contingencies, including what happens in catastrophic events like a house fire. Ensuring proper insurance coverage and understanding the terms of the agreement can help protect both the homeowner’s and Unison’s financial interests.