Should I Accept the First Offer the Insurance Company Makes For My Rental Property?

The devastating January 2025 Los Angeles wildfire left many property owners grappling with significant losses, including damage or destruction of rental buildings. Fires such as the Palisades fire, Altadena fire, and Eaton fire contributed to widespread devastation, leaving many questioning how to handle insurance claims. If you are a property owner dealing with insurance claims, you may be wondering whether to accept the first offer the insurance company makes. While it may be tempting to settle quickly, it is essential to carefully evaluate the offer before making a decision. This article explores the necessary steps to ensure you receive a fair settlement and how to navigate the claims process effectively. Consulting our fire insurance lawyer can help you understand your legal options.

Understanding Your Policy Coverage

Before responding to the first offer the insurance company makes, thoroughly review your insurance policy to understand the scope of your coverage. Policies often include provisions for replacement costs, lost rental income, and additional expenses related to rebuilding. Many policies also include clauses regarding temporary housing costs for tenants displaced by the wildfire, which should be factored into the claim. Rental properties affected by the Malibu fire and Topanga fire may have suffered different levels of destruction, requiring individualized insurance assessments. Our wildfire insurance attorney can help assess whether your policy terms are being honored appropriately. Ensure that the offered settlement aligns with the policy’s terms and covers all aspects of your loss, including both structural and financial components.

Additionally, many insurance policies include clauses related to debris removal, temporary security for damaged properties, and extended loss of income protection. Property owners should scrutinize their policy documents to determine what is covered and whether the initial offer adequately compensates for these additional expenses. In many cases, insurers may not automatically include these costs in their first settlement offer, necessitating a more detailed negotiation. If you own a rental property, ensuring that your claim covers these aspects is crucial for long-term financial stability.

Evaluating the First Offer the Insurance Company Makes

Insurance companies often start with a lower settlement offer, expecting some negotiation. This initial offer is typically a lowball offer because insurers anticipate that rental property owners will counter with a higher demand. By doing so, insurance companies aim to minimize payouts while leaving room for negotiation. Their initial assessment may not fully account for hidden damages, increased construction costs, or the full extent of business interruption. The cost of rebuilding a rental building may be significantly higher due to post-wildfire demand for labor and materials, which insurers may not fully consider in their initial estimates. Consider obtaining an independent appraisal or hiring a public adjuster to ensure you receive a fair and comprehensive evaluation of the loss. Additionally, property owners should gather multiple contractor quotes to compare with the insurance estimate to verify whether it aligns with current market rates. The aftermath of the Hurst fire has shown that insurance estimates do not always reflect the true cost of rebuilding. Our fire insurance claim attorney can negotiate with insurers to ensure fair compensation.

Moreover, property owners should also consider the timeline of their claim. Insurance companies may delay processing claims, which can impact your ability to begin rebuilding. If your rental property was damaged, delays in claim processing could mean months of lost rental income. Our California fire lawyer can assist in expediting claim resolutions by holding insurers accountable for unnecessary delays. Their initial assessment may not fully account for hidden damages, increased construction costs, or the full extent of business interruption. The cost of rebuilding a rental building may be significantly higher due to post-wildfire demand for labor and materials, which insurers may not fully consider in their initial estimates. Consider obtaining an independent appraisal or hiring a public adjuster to ensure you receive a fair and comprehensive evaluation of the loss. Additionally, property owners should gather multiple contractor quotes to compare with the insurance estimate to verify whether it aligns with current market rates. The aftermath of the Hurst fire has shown that insurance estimates do not always reflect the true cost of rebuilding. Our fire insurance claim attorney can negotiate with insurers to ensure fair compensation.

Moreover, property owners should also consider the timeline of their claim. Insurance companies may delay processing claims, which can impact your ability to begin rebuilding. If your rental property was damaged, delays in claim processing could mean months of lost rental income. Our California fire lawyer can assist in expediting claim resolutions by holding insurers accountable for unnecessary delays.

Steps to Strengthen Your Claim

- Conduct a Thorough Damage Assessment: Take detailed photographs and videos of all damage, including structural components, personal property, and exterior elements. This step is especially important for rental properties, where damage may extend beyond the building itself and impact tenants.

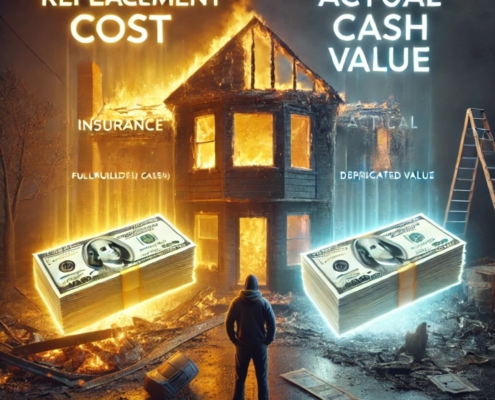

- Review and Understand Your Policy: Confirm the exact coverage details, such as actual cash value (ACV) versus replacement cost value (RCV) settlements.

- Seek an Independent Appraisal: Hire a licensed contractor or public adjuster to provide an unbiased damage estimate. Comparing these assessments with the first offer the insurance company makes can help determine whether the settlement is fair.

- Calculate Your Losses Beyond Structure Damage: Consider loss of rental income, additional temporary housing costs for tenants, and property depreciation.

- File a Comprehensive Claim: Submit a claim with all relevant documentation, receipts, and contractor estimates to ensure a robust request for compensation. Our fire damage insurance claim attorney can help ensure your claim is filed properly and includes all eligible losses.

- Stay Organized: Keep a record of all communication with the insurance company, including emails, letters, and phone call summaries, to provide evidence of any discrepancies or delays in the claims process.

Negotiation Strategies

- Document Everything: Maintain detailed records of damages, repair estimates, and lost rental income to support your claim. Having well-documented proof can help counter a lower-than-expected settlement offer.

- Seek Professional Advice: Consult with attorneys, adjusters, or financial advisors experienced in wildfire-related claims. These professionals understand insurance loopholes and can guide you through a more effective negotiation process. Our California wildfire lawyer specializes in advocating for fair settlements.

- Don’t Rush: Avoid accepting the first offer the insurance company makes under pressure. Take time to review and negotiate for a more accurate and fair settlement. Many property owners may feel the need to accept an initial offer to expedite the rebuilding process, but patience often leads to a more comprehensive payout.

- Understand the Appeals Process: If your claim is denied or undervalued, you have the right to appeal. Insurers must provide an explanation of their decision, and policyholders can counter with additional documentation or an independent assessment. Our Los Angeles wildfire lawyer can help navigate the appeals process effectively.

- Consider Mediation: If a dispute arises, mediation may be a viable option before pursuing litigation. Mediation allows both parties to negotiate with the help of a neutral third party, potentially resulting in a quicker resolution.

Legal Considerations

In some cases, insurance companies may undervalue claims or delay payments. If negotiations stall, legal action might be necessary to secure proper compensation. Consulting our California fire attorney who specializes in insurance claims and property loss can help you navigate this process effectively. Legal professionals can also identify whether bad faith insurance practices are at play, such as unjustified claim denials, delayed responses, or insufficient settlement amounts. Some property owners may also explore filing a lawsuit against the insurer if settlement negotiations remain stagnant. Our SoCal fire attorney has experience handling fire insurance disputes and can provide legal guidance tailored to your case.

Additionally, fire-related legal claims can be complex due to overlapping state and federal regulations. Our Eaton fire attorney can provide insight into how local laws impact wildfire insurance claims and what additional legal remedies may be available to affected property owners. If your rental building was impacted by fire, seeking legal assistance can help ensure that your insurance claim fully covers reconstruction costs and lost income.

Conclusion

While accepting the first offer the insurance company makes might seem like a quick solution, it is often in your best interest to conduct due diligence and negotiate for a fair settlement. By understanding your policy, evaluating the offer, and seeking expert advice, you can maximize your claim and ensure adequate compensation for your rental building loss. Ensuring a fair settlement will help you rebuild and recover after the loss of your rental building. Property owners should be proactive, informed, and persistent in their negotiations to achieve the best possible outcome. Our Eaton fire lawyer and Altadena fire lawyer are available to assist with wildfire-related insurance claims, ensuring you receive the settlement you deserve. Consulting our Los Angeles wildfire attorney can further protect your rights and ensure the insurance company meets its obligations.