The Impact on High-Value Areas

The devastating wildfires that swept through California in January 2025 have had catastrophic effects on homeowners, especially in areas such as Pacific Palisades, Altadena, Eaton Canyon, Malibu, Topanga, and Sylmar. As the fires claimed thousands of homes and properties, many homeowners are now grappling with an additional crisis: their insurance companies are offering settlements that are significantly lower than the actual value of their homes.

Palisades Fire: The Palisades Fire, which ignited on January 7, 2025, consumed over 23,700 acres and devastated the affluent Pacific Palisades neighborhood. Known for its high-value properties, with median home prices around $3 million, the fire destroyed at least 6,770 structures and damaged 904 more. Insured losses in this area alone are estimated to exceed $28 billion, reflecting the immense financial toll on homeowners. In such situations, working with our fire insurance lawyer or our wildfire insurance attorney can help homeowners navigate complex claims processes and disputes effectively.

Altadena and Eaton Fires: The Eaton Fire ravaged parts of Altadena and Pasadena, burning over 14,100 acres. Altadena, where median home values are around $1.3 million, saw extensive losses, with 9,418 structures destroyed and 1,073 damaged. Reconstruction costs for this area are projected to surpass $13 billion. Homeowners in these neighborhoods, many of whom invested heavily in their properties, are now facing significant challenges with their insurance claims. For those affected by the Eaton Fire, consulting our Eaton fire attorney or our fire damage insurance claim lawyer can provide critical support in negotiating fair settlements.

Malibu and Topanga Fires: Fires in Malibu and Topanga, areas renowned for their scenic beauty and luxury homes, resulted in the destruction of numerous beachfront and hillside properties. These homes, often valued in the multi-million-dollar range, contribute significantly to the overall financial impact of the fires. The emotional toll on homeowners is compounded by insurance settlements that fail to cover the full cost of rebuilding. Engaging our Malibu fire attorney or our wildfire insurance lawyer can help homeowners in these regions address underinsurance challenges.

Hurst Fire: In Sylmar, the Hurst Fire burned approximately 700 acres. While the scale of destruction was smaller compared to other areas, the impact on local communities remains substantial, with homeowners in this area also facing underinsurance issues. Seeking assistance from our SoCal fire attorney or our Los Angeles wildfire lawyer can be a valuable step in resolving claims and ensuring fair compensation.

The Underinsurance Crisis

Underinsurance occurs when a homeowner’s insurance policy does not adequately cover the costs of rebuilding or repairing a property after a disaster. This issue is particularly acute in high-value areas like Pacific Palisades, Malibu, and Altadena, where soaring home values and rising construction costs have created a significant gap between policy limits and actual rebuilding expenses. Factors contributing to underinsurance include:

- Outdated Policy Limits: Many homeowners have not updated their policies to reflect current property values or construction costs.

- Increased Building Costs: Post-disaster demand for materials and labor often drives up construction prices, leaving homeowners unable to rebuild with the settlements offered.

- Unreported Home Improvements: Renovations or additions to homes that were not reported to insurers may not be covered, further reducing settlement amounts. Consulting our fire insurance claim attorney can help homeowners ensure that these gaps are addressed during the claims process.

What to Do if the Insurance Settlement is Too Low

When a homeowner’s insurance settlement is insufficient to cover damages, several steps can be taken:

- Understand the 80% Rule in Home Insurance: Many insurance policies include a requirement that the home be insured for at least 80% of its replacement cost. If this threshold isn’t met, the insurer may not fully cover damages. Homeowners should review their policy to determine whether they meet this requirement. Our California fire attorney can assist in interpreting these policy terms and ensuring compliance.

- Document and Challenge the Settlement: Homeowners should gather comprehensive evidence of the damages, including repair estimates, receipts, and photographs, and use this information to negotiate a higher settlement with their insurer. Engaging our fire damage insurance claim attorney can provide additional leverage in these negotiations.

- Hire An Wildfire Insurance Lawyer: Hiring a Los Angeles wildfire attorney or an insurance attorney experienced in insurance claims can provide valuable expertise in disputing low settlements. Our wildfire insurance attorney specializes in assisting homeowners during such disputes. Additionally, filing a lawsuit for bad faith practices may be necessary if an insurance company deliberately makes lowball settlement offers. Bad faith refers to an insurer’s intentional failure to uphold the terms of the policy, such as underestimating damages, delaying payment, or unjustly denying a claim. Consulting our fire insurance claim lawyer can help homeowners pursue compensation for not only the losses but also the emotional and financial distress caused by these unfair practices.

- Appeal or File a Complaint: If negotiations fail, homeowners can appeal directly to their insurance company or file a complaint with their state’s insurance regulator. Our LA fire attorney can guide homeowners through these legal channels.

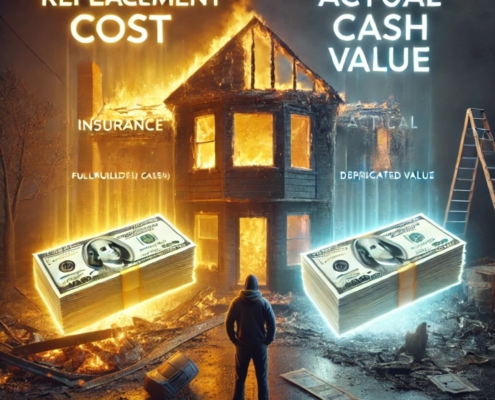

How Insurance Companies Determine Actual Cash Value

Insurance companies calculate the actual cash value (ACV) of a home by considering its replacement cost and subtracting depreciation. Depreciation accounts for the age, wear, and tear of the property. For example, a 20-year-old roof may only receive a fraction of its replacement cost due to its age, even if replacing it costs tens of thousands of dollars. This approach often results in settlements that are significantly lower than the cost to fully rebuild a home, especially for older properties.

In another instance, if a home’s total replacement cost is estimated at $500,000 but years of depreciation reduce its value to $300,000, the homeowner may face a $200,000 gap unless they have replacement cost value (RCV) coverage. Homeowners should be aware of this calculation method and consider policies that offer RCV coverage instead. For personalized advice, consulting our fire insurance claim lawyer can help clarify these calculations and advocate for more accurate valuations.

The 80/20 Rule in Insurance

In insurance, the 80/20 rule often refers to the principle that 80% of claims are filed by 20% of policyholders. While not directly related to home insurance, this principle underscores the importance of understanding policyholder behaviors and risk management. For homeowners, it highlights the need to ensure their coverage aligns with potential risks, particularly in disaster-prone areas. Seeking guidance from our SoCal fire lawyer can help homeowners align their policies with these principles.

Steps for Homeowners Facing Insufficient Settlements

- Review Your Policy: Homeowners should begin by thoroughly reviewing their insurance policy to understand coverage limits, exclusions, and terms.

- Document the Damage: Creating detailed records of the damage—including photographs, videos, and itemized lists—is essential for supporting claims and negotiations.

- Obtain Repair Estimates: Seeking multiple estimates from licensed contractors can provide evidence to challenge low settlement offers.

- Engage in Open Communication: Presenting documentation and contractor estimates to the insurance company can aid in negotiating a higher payout.

- Seek Professional Assistance: If negotiations stall, hiring a public adjuster or attorney experienced in insurance claims can be invaluable. Our California wildfire lawyer can help homeowners navigate disputes and pursue fair settlements. Additionally, homeowners should consider filing lawsuits against potentially liable parties, such as utility companies or municipalities, if negligence contributed to the disaster. For instance, lawsuits against utility companies may be warranted if their infrastructure failures, such as faulty power lines, ignited fires. Similarly, municipalities, including the City of Los Angeles, could face legal action if inadequate fire prevention measures or mismanagement of resources exacerbated the destruction. Consulting our California wildfire attorney or Los Angeles fire attorney can provide clarity and guidance on these legal options.

- Know Your Rights and Options: Familiarize yourself with state laws and protections for insurance policyholders. Many states have consumer protection agencies that assist in resolving disputes with insurers. Our Los Angeles wildfire attorney can represent homeowners in these cases effectively.

Legal Recourse and Advocacy

In cases where insurance companies fail to provide adequate compensation, legal action may be necessary. For example, some homeowners affected by the Palisades Fire have filed lawsuits against their insurers, alleging bad faith practices and insufficient settlement offers. Additionally, lawsuits may be filed against utility companies, such as those responsible for maintaining power lines, if evidence suggests that negligence or faulty infrastructure contributed to the ignition of the fire. Similarly, municipalities like the City of Los Angeles may face legal action if they failed to implement adequate fire prevention measures, mismanaged resources, or contributed to the severity of the disaster. Filing such lawsuits serves to hold potentially liable parties accountable and may provide additional compensation to support the rebuilding process. Our LA fire lawyer or California wildfire attorney can provide the legal expertise required to pursue these cases.

Insights into Preventative Measures

Homeowners can take several steps to prevent underinsurance and better prepare for potential disasters in the future:

- Regularly Update Policies: Ensure that your policy reflects the current replacement cost of your home and accounts for any improvements or changes.

- Conduct Professional Home Appraisals: Regular appraisals can provide an accurate estimate of your home’s value, helping to ensure your coverage is adequate.

- Explore Extended Replacement Cost Coverage: Many insurers offer endorsements that cover rebuilding costs exceeding your policy limits.

- Build a Home Inventory: Maintain a detailed inventory of personal property, including photos, descriptions, and receipts when possible. This will streamline claims and ensure full compensation for losses.

- Consider Risk-Specific Endorsements: Policies tailored to wildfire-prone areas, for example, may include enhanced protections for fire damage and mandatory evacuation costs.

The Bigger Picture: Policyholder Advocacy and Systemic Changes

The challenges faced by homeowners during the January 2025 wildfires underscore the need for systemic improvements in the insurance industry. Policymakers, insurers, and consumer advocates must work together to:

- Address Gaps in Coverage: Review and refine policy structures to ensure homeowners are adequately protected.

- Enhance Transparency: Improve clarity around how premiums are calculated, particularly regarding replacement costs versus actual cash value.

- Educate Homeowners: Provide resources to help homeowners understand their coverage and make informed decisions. Our California fire lawyer or wildfire insurance attorney can play a critical role in educating policyholders about their rights.

Conclusion

The January 2025 wildfires have highlighted the vulnerabilities in the current insurance system, especially for homeowners in high-value areas. The destruction wrought by fires in Pacific Palisades, Altadena, Malibu, and beyond underscores the importance of adequate coverage and proactive measures. As communities rebuild, addressing the systemic issue of underinsurance is critical to helping homeowners recover. By regularly updating policies, understanding key insurance principles like the 80% rule, and seeking professional guidance when disputes arise, homeowners can navigate these challenges effectively and advocate for fair compensation in the wake of disasters. Furthermore, systemic reforms and increased transparency will be essential in creating a more resilient and equitable insurance landscape for all.