Does homeowners insurance pay off your mortgage if the house is lost?

Owning a home is one of the biggest financial commitments most people make, and a mortgage typically accompanies this investment. Homeowners insurance provides critical protection against disasters, including fires, but many homeowners wonder: Does insurance pay off your mortgage if your house burns down?

The short answer is no, homeowners insurance does not directly pay off your mortgage in the event of a fire. Instead, it provides funds to rebuild or repair the home, ensuring that the property remains livable and valuable. However, in certain circumstances, the insurance payout could be used to pay off the mortgage if you choose not to rebuild.

The increasing number of devastating wildfires in California, such as the Palisades Fire and the Altadena Fire, has raised concerns among homeowners about whether their insurance coverage is sufficient to rebuild or pay off their remaining mortgage balance. Unfortunately, many homeowners face challenges when dealing with their insurance companies, leading them to seek help from our fire insurance lawyer to navigate the claims process and ensure they receive the compensation they deserve.

The challenges of insurance claims become even more acute in areas severely impacted by the wildfires:

-

- Pacific Palisades: The Palisades Fire burned over 23,713 acres starting on January 7, 2025, destroying homes and cultural landmarks.

- Altadena: The Eaton Fire devastated this community, destroying thousands of structures, including historic restaurants and businesses along Lake Avenue.

- Malibu: Parts of Malibu, known as the Malibu fire, suffered significant losses as the Palisades Fire extended into the area, leading to the destruction of beachfront properties.

- Topanga: This community faced evacuations and property losses as the Topanga fire spread through the region.

- San Fernando Valley: The Hurst Fire burned approximately 799 acres near San Fernando, causing evacuations and damage to properties.

These widespread damages amplify the difficulties for businesses trying to quantify their losses and file comprehensive claims. Working with a Los Angeles fires lawyer or an Altadena fire lawyer can help streamline the claims process and ensure a fair settlement.

This article explores how insurance policies work after a fire, how the mortgage lender is involved, and what happens if your insurance payout is insufficient to cover your mortgage.

How Homeowners Insurance Works After a Fire

Homeowners insurance is designed to protect both you and your mortgage lender by covering the costs associated with rebuilding your home. Most standard homeowners insurance policies include dwelling coverage, which pays for the repair or rebuilding of your house if it is damaged or destroyed by a covered peril, such as a fire.

When your house burns down, the insurance company assesses the damage and determines how much money you are entitled to based on the coverage limits in your policy.

Key Elements of Homeowners Insurance Coverage After a Fire

- Dwelling Coverage – Covers the cost of rebuilding or repairing your home up to the policy limit.

- Other Structures Coverage – Pays for repairs to detached structures like garages, sheds, or fences.

- Personal Property Coverage – Provides compensation for lost or damaged belongings inside the home.

- Additional Living Expenses (ALE) Coverage – Covers temporary housing, meals, and other costs if you are displaced.

- Liability Protection – Covers legal expenses if someone is injured on your property due to the fire.

While these coverages help restore your home and belongings, they do not automatically pay off your mortgage. Many homeowners affected by the Eaton Fire and Topanga Fire have discovered the hard way that their insurance policies are structured to rebuild rather than eliminate existing debt. Those who encounter resistance from their insurance companies often turn to our fire insurance claim attorney or our fire damage insurance claim lawyer to fight for fair settlements.

What Happens to Your Mortgage After a Fire?

If your home is destroyed by a fire, your mortgage does not automatically disappear. You are still responsible for making your monthly mortgage payments. Even though your home may be unlivable, the loan remains in effect unless it is fully paid off through insurance funds or other means.

However, since lenders have a financial interest in your property, they are often listed as loss payees on your homeowners insurance policy. This means:

- The Insurance Company Issues the Payout to Both You and Your Lender

- Instead of cutting a check directly to you, the insurance company usually writes the check payable to both you and your mortgage lender.

- This ensures that the funds are used to repair or rebuild the home rather than being spent elsewhere.

- Your Mortgage Lender May Hold the Insurance Proceeds in an Escrow Account

- Most lenders require you to repair or rebuild the home rather than simply taking the money and walking away.

- The lender will likely release the funds in increments as construction progresses, ensuring the home is restored.

- If You Choose Not to Rebuild, the Lender May Require You to Pay Off the Mortgage

- If you decide not to rebuild or sell the property as-is, the lender may insist that the insurance payout be used to pay off the mortgage first.

- If the payout exceeds your mortgage balance, you may keep the remaining funds.

After the Malibu Fire, many homeowners faced difficult choices. Some used their insurance payouts to rebuild, while others decided to sell their land and move elsewhere, using the funds to settle their mortgage debt. However, those who were underinsured were left struggling to cover the remaining balance of their loans, often turning to our California fire lawyer for legal assistance.

Does Insurance Ever Pay Off the Mortgage?

While homeowners insurance is designed to rebuild rather than pay off your loan, there are scenarios where the insurance payout can be used to eliminate mortgage debt:

1. You Choose to Use the Insurance Money to Pay Off the Mortgage

If your insurance payout is large enough, you could decide to pay off your mortgage in full instead of rebuilding. This is only an option if your policy payout covers your remaining loan balance.

2. You Have Mortgage Protection Insurance

Mortgage protection insurance (MPI) is a separate policy that directly pays off your mortgage if your home is destroyed, you pass away, or you become disabled. Unlike homeowners insurance, this type of coverage is specifically designed to settle your mortgage in extreme circumstances.

3. The Lender Requires It

In some cases, if you choose not to rebuild, your lender may require you to use the insurance payout to pay down or pay off the mortgage. This is more common if the home is a total loss and rebuilding is not financially viable.

After the Hurst Fire, some affected homeowners found that their insurance policies did not provide enough coverage to rebuild, forcing them to consider selling their property. In those cases, lenders often required insurance proceeds to be applied toward the remaining mortgage balance before any remaining funds were released to the homeowner. Many turned to our Los Angeles wildfire attorney or our SoCal fire lawyer to help negotiate with their lenders and insurance providers.

What If the Insurance Payout Is Less Than Your Mortgage Balance?

One of the biggest concerns homeowners face after a fire is what happens if the insurance payout is insufficient to cover the remaining mortgage balance?

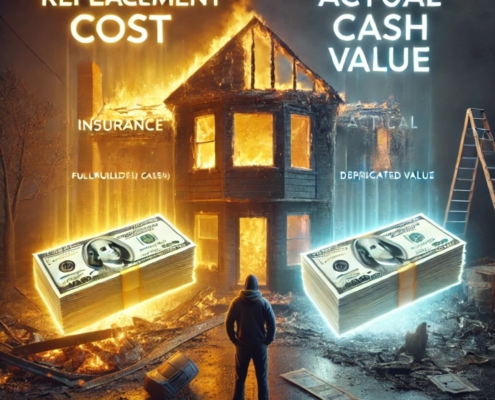

- If your dwelling coverage limit is lower than the actual cost to rebuild, you may find yourself in a situation where the insurance payout does not cover the entire loss.

- Many homeowners are underinsured because they only buy coverage equal to their home’s purchase price rather than its full replacement cost.

- Even if your home is completely destroyed, your mortgage does not disappear. If the insurance payout falls short, you must continue making mortgage payments unless other arrangements are made.

Conclusion: Does Insurance Pay Off Your Mortgage If Your House Burns Down?

In most cases, homeowners insurance does not directly pay off your mortgage if your house burns down. Instead, the insurance payout is intended to repair or rebuild your home, ensuring that your property remains intact and your lender’s interest is protected.

However, if you choose not to rebuild, your mortgage lender may require you to use the insurance payout to settle the loan. If your insurance proceeds exceed your mortgage balance, you may keep the remaining funds.

To fully protect yourself, consider mortgage protection insurance if you want a policy that will pay off your loan in case of home destruction, disability, or death.

Ultimately, understanding your policy coverage, working with your insurance provider, and communicating with your lender will help you navigate the difficult situation of losing a home to fire, as many have experienced after the Palisades Fire, Altadena Fire, Eaton Fire, Malibu Fire, Topanga Fire, and Hurst Fire. If you are facing claim denials or delays, our fire insurance attorney or our California wildfire lawyer can help you fight for the compensation you deserve.