https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/02/Unison-agreement-house-burns-down.jpg

1295

1294

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-02-10 17:13:142025-02-10 17:13:15Unison Agreement: What Happens If the House Burns Down?

https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/02/Unison-agreement-house-burns-down.jpg

1295

1294

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-02-10 17:13:142025-02-10 17:13:15Unison Agreement: What Happens If the House Burns Down? https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/02/insurance-offer-for-rental-property.jpg

1291

1290

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-02-02 14:38:382025-02-02 14:38:39Property owners should not accept the first offer the insurance company makes for the loss of my rental building.

https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/02/insurance-offer-for-rental-property.jpg

1291

1290

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-02-02 14:38:382025-02-02 14:38:39Property owners should not accept the first offer the insurance company makes for the loss of my rental building. https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/02/insurance-first-offer.jpg

1298

1297

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-02-02 14:15:432025-02-02 14:18:02Should You Accept the First Insurance Offer After the January 2025 Los Angeles Wildfire?

https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/02/insurance-first-offer.jpg

1298

1297

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-02-02 14:15:432025-02-02 14:18:02Should You Accept the First Insurance Offer After the January 2025 Los Angeles Wildfire? https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/02/insurance-low-ball-offer.jpg

1166

1172

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-02-01 14:24:042025-02-01 14:24:48What to do if home insurance settlement is too low?

https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/02/insurance-low-ball-offer.jpg

1166

1172

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-02-01 14:24:042025-02-01 14:24:48What to do if home insurance settlement is too low? https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/wildfire-assistance.jpg

1230

1232

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-30 16:38:152025-01-30 16:38:23Everything you need to know about applying for FEMA wildfire assistance in California

https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/wildfire-assistance.jpg

1230

1232

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-30 16:22:022025-02-07 20:03:35How to Apply for Wildfire Assistance in California After the January 2025 Los Angeles Wildfires

https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/wildfire-assistance.jpg

1230

1232

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-30 16:38:152025-01-30 16:38:23Everything you need to know about applying for FEMA wildfire assistance in California

https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/wildfire-assistance.jpg

1230

1232

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-30 16:22:022025-02-07 20:03:35How to Apply for Wildfire Assistance in California After the January 2025 Los Angeles Wildfires https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/house-burn-mortgage-2.jpg

1231

1226

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-30 15:59:232025-02-01 13:43:23Does Insurance Pay Off Your Mortgage If Your House Burns Down?

https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/house-burn-mortgage-2.jpg

1231

1226

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-30 15:59:232025-02-01 13:43:23Does Insurance Pay Off Your Mortgage If Your House Burns Down? https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/house-burn-mortgage.jpg

1235

1234

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-30 15:45:422025-01-30 15:53:03What happens if your house burns down and you have a mortgage?

https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/house-burn-mortgage.jpg

1235

1234

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-30 15:45:422025-01-30 15:53:03What happens if your house burns down and you have a mortgage? https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/insurnace-payout-after-wildfire.jpg

1300

1296

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-30 15:18:282025-01-30 15:22:14Do I Have to Pay My Mortgage After My House Burns Down?

https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/insurnace-payout-after-wildfire.jpg

1300

1296

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-30 15:18:282025-01-30 15:22:14Do I Have to Pay My Mortgage After My House Burns Down? https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/lawyer-wildfire.jpg

1288

1290

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-29 13:13:532025-01-29 13:13:53Luật Sư Đại Diện Vụ Cháy Eaton, Kiện Tụng Liên Quan Đến Cháy Rừng Los Angeles & Altadena

https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/lawyer-wildfire.jpg

1288

1290

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-29 13:13:532025-01-29 13:13:53Luật Sư Đại Diện Vụ Cháy Eaton, Kiện Tụng Liên Quan Đến Cháy Rừng Los Angeles & Altadena https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/construction-house-home.jpg

1299

1299

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-29 13:07:542025-01-29 13:07:54伊頓火災律師、洛杉磯和阿爾塔迪納野火訴訟

https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/construction-house-home.jpg

1299

1299

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-29 13:07:542025-01-29 13:07:54伊頓火災律師、洛杉磯和阿爾塔迪納野火訴訟 https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Bradsmallsize.jpg

311

400

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-28 16:00:212025-01-28 16:00:21イートン火災弁護士 、ロサンゼルス・アルタデナ地区山火事訴訟

https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Bradsmallsize.jpg

311

400

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-28 16:00:212025-01-28 16:00:21イートン火災弁護士 、ロサンゼルス・アルタデナ地区山火事訴訟 https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/replacement-cost-vs-actual-cash-value.jpg

1301

1297

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

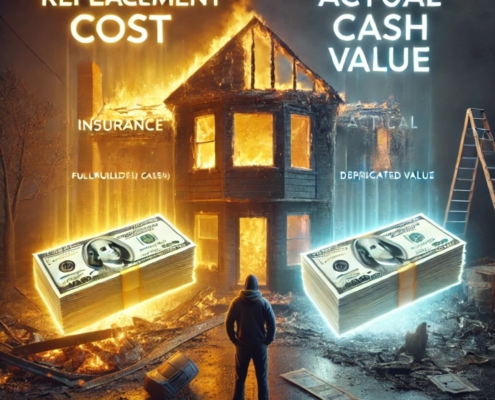

Nakase2025-01-25 14:55:412025-01-25 15:00:09Replacement Cost vs. Actual Cash Value: A Guide for Homeowners Recovering from Wildfire Losses

https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/replacement-cost-vs-actual-cash-value.jpg

1301

1297

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-25 14:55:412025-01-25 15:00:09Replacement Cost vs. Actual Cash Value: A Guide for Homeowners Recovering from Wildfire Losses https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/insurance-low-ball-offer.jpg

1302

1298

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-25 13:57:592025-01-25 13:59:06My home owner insurance company is offering less money than what my home is worth.

https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/insurance-low-ball-offer.jpg

1302

1298

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-25 13:57:592025-01-25 13:59:06My home owner insurance company is offering less money than what my home is worth. https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/Fair-Plan-broke-no-money.jpg

1298

1296

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

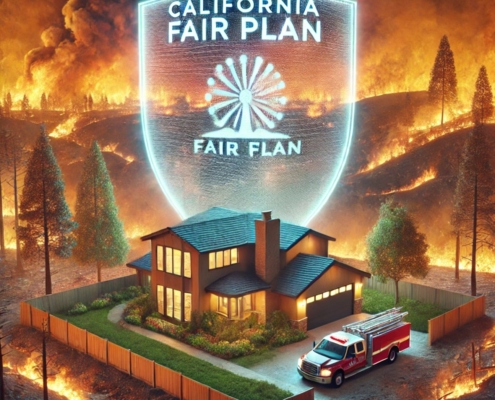

Nakase2025-01-25 13:27:132025-01-25 13:41:57Will California’s FAIR Plan have enough cash to pay wildfire claims?

https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/Fair-Plan-broke-no-money.jpg

1298

1296

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-25 13:27:132025-01-25 13:41:57Will California’s FAIR Plan have enough cash to pay wildfire claims? https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/fair-plan-offer-little-money.jpg

1300

1294

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-25 12:57:102025-01-25 14:03:36What to do when the FAIR Plan offers little money?

https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/construction-house-home.jpg

1299

1299

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-25 12:32:182025-01-25 12:33:20Why does the Fair plan pay so little?

https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/fair-plan-offer-little-money.jpg

1300

1294

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-25 12:57:102025-01-25 14:03:36What to do when the FAIR Plan offers little money?

https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/construction-house-home.jpg

1299

1299

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-25 12:32:182025-01-25 12:33:20Why does the Fair plan pay so little? https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/Fair-Plan-wildfire.jpg

1291

1291

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-23 20:54:542025-01-23 23:06:30Does the FAIR Plan Include Wildfire Protection for California 2025 wildfires?

https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/Fair-Plan-wildfire.jpg

1291

1291

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-23 20:54:542025-01-23 23:06:30Does the FAIR Plan Include Wildfire Protection for California 2025 wildfires? https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/California-FAIR-plan-3.jpg

1297

1295

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-23 17:21:082025-01-23 19:37:41What does the CA Fair Plan not cover?

https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/California-FAIR-plan-3.jpg

1297

1295

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-23 17:21:082025-01-23 19:37:41What does the CA Fair Plan not cover? https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/California-Fair-Plan-peril.jpg

1300

1299

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-23 16:37:322025-01-23 19:36:53What perils does the California Fair Plan cover?

https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/California-Fair-Plan-peril.jpg

1300

1299

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-23 16:37:322025-01-23 19:36:53What perils does the California Fair Plan cover? https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/california-FAIR-plan.jpg

1301

1298

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-23 16:06:452025-01-23 19:38:08California’s FAIR Plan Will Not Have Enough Money to Pay Wildfire Claims

https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/california-FAIR-plan.jpg

1301

1298

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-23 16:06:452025-01-23 19:38:08California’s FAIR Plan Will Not Have Enough Money to Pay Wildfire Claims https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/court-wildfire-lawsuit.jpg

1299

1295

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-22 23:44:072025-01-23 19:39:11Wildfire Lawsuit: LA Fires

https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/court-wildfire-lawsuit.jpg

1299

1295

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-22 23:44:072025-01-23 19:39:11Wildfire Lawsuit: LA Fires https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/wildfire-payout.jpg

1300

1299

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-22 23:44:022025-01-23 19:39:44Wildfire Lawsuit Payout Per Person

https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/wildfire-payout.jpg

1300

1299

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-22 23:44:022025-01-23 19:39:44Wildfire Lawsuit Payout Per Person https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/wildfire-first-responders.jpg

1299

1298

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-22 21:56:562025-01-23 19:40:38California Wildfires – Employer Guidelines for Employees Safety and Legal Responsibilities

https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/lawyer-wildfire.jpg

1288

1290

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-22 21:46:032025-01-23 19:41:07Wildfire Attorney

https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/wildfire-first-responders.jpg

1299

1298

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-22 21:56:562025-01-23 19:40:38California Wildfires – Employer Guidelines for Employees Safety and Legal Responsibilities

https://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2025/01/lawyer-wildfire.jpg

1288

1290

Nakase

http://california-business-lawyer-corporate-lawyer.com/wp-content/uploads/2022/05/Nakase-Wade-logo-transparent-200x54px.png

Nakase2025-01-22 21:46:032025-01-23 19:41:07Wildfire Attorney