Introduction

The devastating wildfires that swept through Los Angeles in January 2025, including the Palisades, Altadena, Eaton, Malibu, Topanga, and Hurst fires, have left countless homeowners grappling with the destruction of their properties. These fires have caused extensive damage, forcing individuals to face the challenging processes of insurance claims and rebuilding their lives.

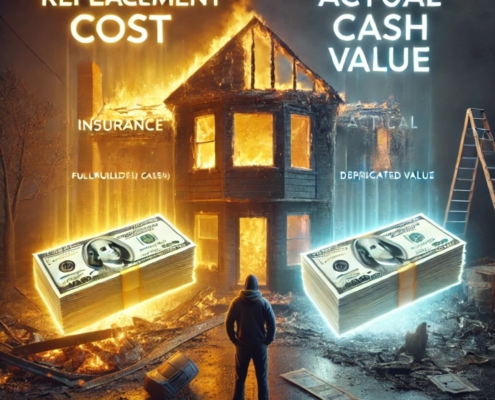

A critical factor in successfully navigating this recovery process is understanding the difference between Replacement Cost Value (RCV) and Actual Cash Value (ACV) in homeowners insurance policies. When purchasing insurance, policyholders typically choose to insure their property based on either its “replacement cost” or its “actual cash value.”

The distinction between these two terms lies in how insurance policies reimburse policyholders for property damage after a covered loss. Replacement Cost Value (RCV) pays the full cost to repair or replace damaged property with new materials of similar kind and quality, without considering depreciation. In contrast, Actual Cash Value (ACV) pays the depreciated value of your property at the time of loss, factoring in age, wear, and tear.

For homeowners recovering from the wildfires, understanding these differences is essential for making informed decisions about their insurance claims and ensuring the best possible outcome during this difficult time.

Replacement Cost vs. ACV: What is the difference?

Home insurance policies typically define the reimbursement for damaged or destroyed property in two main ways:

- Replacement Cost: A home replacement cost pays for the cost of replacing damaged property with new items of similar kind and quality. It does not factor in depreciation. For example, if your kitchen appliances were destroyed in the fire, replacement cost coverage would reimburse you the amount needed to purchase new appliances of comparable quality at current market prices.

- Actual Cash Value: Actual Cash Value coverage, on the other hand, reimburses the value of the damaged property at the time of loss, accounting for depreciation. This means the payout reflects the item’s current market value rather than the cost to replace it. For instance, a 15-year-old roof with a 20-year lifespan would be valued based on its remaining five years of usability. Other items subject to depreciation include HVAC systems, plumbing, electrical wiring, flooring materials, cabinetry, and exterior paint, all of which lose value over time due to wear and tear or outdated functionality.

Choosing between these coverages can significantly impact your financial recovery after a disaster. While replacement cost coverage generally results in higher premiums, it provides more comprehensive protection, ensuring that you can rebuild or replace items without significant out-of-pocket expenses. Conversely, ACV coverage often comes with lower premiums but may leave policyholders with a financial gap when replacing depreciated items.

Is replacement cost or actual cash value better? Replacement cost coverage is generally better for homeowners in high-risk areas or those with properties featuring high-value or custom elements. For example, a homeowner in Malibu with a custom-designed home may find replacement cost essential to restore high-end materials and intricate designs. Actual Cash Value, on the other hand, may suffice for those looking to reduce premium costs but leaves significant financial gaps due to depreciation, such as the inability to fully replace aged cabinetry or flooring.

What is the 80% rule in insurance? The 80% rule requires homeowners to carry insurance coverage equal to at least 80% of their home’s replacement cost to receive full reimbursement for a claim. For instance, if a homeowner in Altadena has a replacement cost of $500,000 but only insures for $350,000, they may receive only a prorated payout, leaving them with substantial out-of-pocket expenses.

Is the replacement cost usually higher than the market value? Yes, replacement cost is often higher than the market value. For example, in Topanga, a property’s market value might be $750,000 due to its location, but the replacement cost could exceed $1 million because of unique architectural elements and current construction costs.

How do you calculate ACV from replacement cost? ACV is calculated by subtracting depreciation from the replacement cost. For instance, if a roof costs $20,000 to replace but has depreciated by 50% due to its age, the ACV payout would be $10,000. A homeowner in Hurst might encounter this scenario when filing a claim for an older home’s worn-out features.

How is home replacement cost calculated? Home replacement cost is determined by evaluating factors such as square footage, construction materials, labor costs, and any special features. For example, a home in the Palisades might require higher-end materials and more skilled labor, leading to a higher replacement cost compared to suburban homes in less affluent areas.

What is the difference between replacement cost and agreed value? Replacement cost provides coverage based on the cost of repairing or replacing property without depreciation. Agreed value, however, is a pre-determined amount agreed upon by the insurer and policyholder. For instance, a historical home in Eaton might have an agreed value due to its unique architecture, ensuring its restoration to a specific standard regardless of market fluctuations.

Can you have both agreed value and replacement cost? Yes, some policies allow a combination of agreed value and replacement cost. For example, a homeowner in Malibu may have an agreed value for rare art or antiques and replacement cost for the structure itself.

Is replacement cost the same as appraised value? No, replacement cost and appraised value are different. Replacement cost refers to the amount needed to rebuild the home, while appraised value considers the property’s market value, including land and location factors. For instance, in Topanga, the land might significantly increase appraised value, but replacement cost focuses solely on rebuilding the structure.

How to Calculate the Replacement Cost of Your Home

Calculating the replacement cost of your home ensures that you have adequate insurance coverage to rebuild in case of disaster. Follow these steps to determine an accurate estimate:

- Measure Your Home’s Square Footage: Begin by determining the total square footage of your home, including any additional spaces such as finished basements or detached structures.

- Identify Construction Costs in Your Area: Research the average construction costs per square foot in your location. For example, in Southern California, rebuilding costs may range from $200 to $400 per square foot depending on the type of construction and finishes.

- Factor in Custom Features: Include costs for any custom or high-end features in your home, such as luxury flooring, high-quality cabinetry, or specialty roofing materials.

- Consider Labor and Material Costs: Account for fluctuations in labor and material costs, which often increase after widespread disasters like wildfires due to high demand.

- Include Permits and Fees: Add the costs of necessary permits, architectural services, and any other fees required for reconstruction.

- Use Replacement Cost Calculators: Many insurance companies and online tools provide calculators to estimate replacement costs based on your home’s specifics.

- Consult Professionals: Work with contractors, builders, or insurance agents to get precise estimates tailored to your property.

For example, if your 2,500-square-foot home in Los Angeles requires $300 per square foot to rebuild, your estimated replacement cost would be $750,000. Adding in fees for permits and architectural services might raise the total to $800,000 or more.

How to Calculate the Cash Value of Your Home

Calculating the actual cash value (ACV) of your home is essential to understanding how much your insurance policy may pay in the event of a loss. ACV represents the current market value of your home’s structure, accounting for depreciation. Follow these steps to calculate it:

- Determine Replacement Cost: Begin by estimating the cost to rebuild your home, including materials, labor, and any custom features. This is often referred to as the replacement cost. For example, if rebuilding a 2,500-square-foot home in Southern California costs $300 per square foot, the replacement cost would be $750,000.

- Assess Depreciation: Calculate depreciation based on the age and condition of your home’s components. For example, a roof with a 20-year lifespan that is 10 years old has depreciated by 50%. Apply this principle to other components, such as flooring, cabinetry, and HVAC systems.

- Subtract Depreciation from Replacement Cost: Once depreciation is determined, subtract it from the replacement cost. Using the earlier example, if depreciation across all components totals $150,000, the ACV would be $600,000 ($750,000 – $150,000).

- Consider Market Influences: While ACV typically focuses on the structure, market conditions such as local demand and property value trends may also play a role in determining your insurance settlement.

- Consult Your Insurance Policy: Review your policy to understand how your insurer calculates ACV, as methods can vary. Your insurance agent or adjuster can clarify specific details about your coverage.

Calculating ACV helps homeowners anticipate potential gaps in insurance payouts, especially when policies do not cover full replacement costs.

The Impact of the January 2025 Fires

The January 2025 wildfires have had devastating effects on multiple communities, each highlighting critical differences between Replacement Cost and ACV coverage:

- Palisades Fire: The Palisades Fire Consumed over 23,000 acres, causing extensive property damage in affluent neighborhoods where home values often exceed $2 million. For homeowners with ACV policies, depreciation on high-value features such as luxury finishes and custom-built structures has left significant financial gaps, underscoring the value of replacement cost coverage to restore these properties.

- Altadena Fire: The Altadena Fire significantly impacted middle-income households, destroying homes valued between $800,000 and $1.5 million. Many families with Actual Cash Value policies face challenges replacing essential components like roofing and electrical systems due to depreciation, highlighting the inadequacy of ACV in covering full rebuilding costs.

- Eaton Fire: The Eaton Fire approximately 14,000 acres, affecting properties in areas with a mix of high-value homes and historical architecture. Replacement cost coverage becomes especially important here, as restoring unique or historical features can be prohibitively expensive under ACV policies.

- Malibu Fire: The Malibu Fire destroyed multi-million-dollar estates, many homeowners face reconstruction costs far exceeding their policy limits if they were underinsured. ACV policies often fail to account for the true cost of rebuilding homes with high-end materials and intricate designs, leaving homeowners with substantial out-of-pocket expenses.

- Topanga Fire: The Topanga Fire destroyed several remote properties, often with unique architectural designs, making replacement costs unpredictable. Without replacement cost coverage, homeowners are left struggling to rebuild custom features that Actual Cash Value policies devalue significantly due to depreciation.

- Hurst Fire: The Hurst Fire smaller in scale, this fire impacted suburban communities where many homeowners carried standard insurance policies with limited coverage. Replacement cost policies provide a crucial safety net here, ensuring families can afford to rebuild their homes without facing depreciation-related shortfalls.

These fires illustrate the tangible financial challenges posed by ACV policies, particularly when depreciation and rising construction costs reduce the effectiveness of insurance payouts. Replacement cost coverage, while more expensive, provides homeowners with the necessary financial resources to rebuild fully and restore their lives after such devastating events.

In many cases, homeowners with Actual Cash Value policies have found that their insurance payouts are insufficient to cover the cost of rebuilding their homes to pre-loss conditions. This is particularly true for components of the house that are subject to significant depreciation. For instance, HVAC systems, plumbing, electrical wiring, flooring materials, cabinetry, and exterior paint all lose value over time. These items, essential to the rebuilding process, may result in significant out-of-pocket expenses for those without replacement cost coverage.

Depreciation deductions, combined with rising construction costs, have left some families struggling to secure adequate housing, making it evident that replacement cost coverage provides a more comprehensive safety net for homeowners in disaster-prone areas.

Key Considerations for Homeowners

To mitigate financial strain in the aftermath of a disaster, homeowners should carefully evaluate their insurance coverage and consider the following steps:

- Review Policy Limits: Ensure your coverage limits are sufficient to account for current construction costs in your area. Market conditions and inflation can significantly affect rebuilding expenses.

- Consider Endorsements: Explore additional coverage options such as extended or guaranteed replacement cost endorsements, which can provide extra protection against unexpected increases in rebuilding costs.

- Understand Depreciation: For those with ACV policies, understanding how depreciation is calculated can help you anticipate potential gaps in coverage.

- Regularly Update Policies: Periodically update your insurance policy to reflect changes in your home’s value, including renovations or improvements that increase its worth.

- Document Your Property: Maintain an up-to-date inventory of your belongings, including photos and receipts, to streamline the claims process.

Steps to Take if Your Insurance Offer Falls Short

If your insurance company offers less money than you believe you deserve, seeking legal advice from a professional such as our California fire insurance attorney or our Los Angeles wildfire attorney can help you better understand your options. These experts specialize in helping victims of wildfires and other disasters secure fair settlements.

- Request a Detailed Explanation: Ask your insurer for a written explanation of how they arrived at their offer. This can help identify any discrepancies or misunderstandings.

- Hire a Public Adjuster: A licensed public adjuster can review your claim, assess the damage, and negotiate with the insurance company on your behalf.

- Gather Supporting Documentation: Provide additional evidence, such as contractor estimates, receipts, and photographs of your property before and after the damage, to substantiate your claim.

- File a Complaint with Your State Insurance Department: If you believe your insurer is not acting in good faith, file a complaint with the California Department of Insurance or your local regulatory authority.

- Consult Our Fire Insurance Claim Attorney: If all else fails, consult an attorney about filing a lawsuit against your insurance company for bad faith practices. Bad faith occurs when an insurer fails to handle claims fairly or denies benefits without a reasonable basis. Our fire insurance claim lawyer or our wildfire insurance lawyer can help you seek compensation for the underpayment, as well as additional damages.

- Investigate Liability of Utility Companies: In many wildfire cases, utility companies are found to have contributed to the cause of the fire through negligence, such as failing to maintain power lines. Consider joining or filing a lawsuit against the responsible utility company to recover damages not covered by your insurance policy. Our California wildfire attorney or our Eaton fire lawyer can assist in holding utility companies accountable.

Lessons from the January 2025 Wildfires in Los Angeles County

The 2025 fires underscore the importance of selecting the right insurance coverage. Homeowners in high-risk areas should prioritize replacement cost policies, which provide the financial resources needed to rebuild without the burden of depreciation. While these policies come at a higher premium, they offer peace of mind and comprehensive protection.

For those affected by the recent fires, consulting with insurance professionals and advocating for fair settlements are essential steps toward recovery. As rebuilding efforts commence, understanding the intricacies of home insurance can make a significant difference in restoring not only homes but also livelihoods.