Introduction

The January 2025 wildfires in Los Angeles inflicted catastrophic damage, raising significant concerns about the California FAIR Plan’s capacity to adequately cover the extensive losses incurred by homeowners. Victims of the Palisades fire, Altadena fire, Eaton fire, Malibu fire, Topanga fire, and Hurst fire have not only lost their homes but are also confronting the harsh reality of insurance shortcomings. The FAIR Plan, designed as an insurer of last resort, has proven insufficient in the face of such large-scale devastation.

The FAIR Plan’s coverage caps often fall short of actual rebuilding expenses, leaving homeowners responsible for the difference. For instance, if the rebuilding costs exceed the coverage limit, the homeowner must cover the shortfall out of pocket. Exclusion of Additional Living Expenses (ALE): The FAIR Plan does not cover temporary housing costs while a home is being rebuilt, adding financial stress. This exclusion forces homeowners to bear the high cost of securing alternative accommodations. Additionally, rebuilding must comply with modern fire-resistant building codes, which can significantly increase costs, but these upgrades are often not accounted for in FAIR Plan policies.

What is the California FAIR Plan?

The California FAIR Plan was established to provide basic fire insurance for homeowners in high-risk areas who are denied coverage by private insurers. However, it is inherently limited by design, offering only minimal protection. It does not cover liabilities, theft, water damage, or additional living expenses (ALE), leaving homeowners with substantial gaps in coverage during their most vulnerable moments.

Estimated Damages

Catastrophe risk modeling firm KCC estimates that insured losses from the Los Angeles wildfires will amount to around $28 billion, making them the most expensive wildfires in U.S. history. Total economic losses, including uninsured property and broader economic impacts, are projected to reach up to $250 billion. For communities like Malibu, Palisades, and Altadena, the economic toll is staggering. The FAIR Plan’s limited scope means it cannot cover a significant portion of these damages, creating a crisis for homeowners.

Catastrophe risk modeling firm KCC estimates that insured losses from the Los Angeles wildfires will amount to around $28 billion, making them the most expensive wildfires in U.S. history. Total economic losses, including uninsured property and broader economic impacts, are projected to reach up to $250 billion. For communities like Malibu, Palisades, and Altadena, the economic toll is staggering. The FAIR Plan’s limited scope means it cannot cover a significant portion of these damages, creating a crisis for homeowners.

Why Does the FAIR Plan Pay So Little?

Several factors contribute to the FAIR Plan’s inability to meet the needs of affected homeowners:

- Coverage Caps: The FAIR Plan imposes strict limits on coverage amounts, which often fall short of the actual costs required to rebuild homes in high-risk areas. In affluent neighborhoods like Pacific Palisades, where the average cost to rebuild a home is approximately $947,000, coverage caps often leave homeowners facing significant financial gaps. Similarly, in Altadena, where rebuilding costs average around $262,000, the limits are still insufficient. This disparity forces homeowners to pay out of pocket or rely on loans to cover the difference, exacerbating financial strain during an already devastating time.

- Limited Perils Covered: The plan primarily covers fire damage and related perils but excludes protection for theft, water damage, and liability. This limited coverage leaves homeowners vulnerable to additional financial strain.

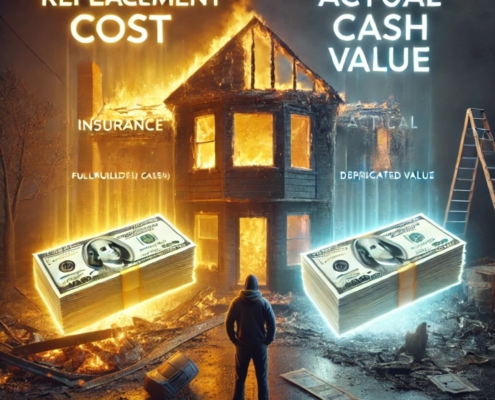

- Actual Cash Value vs. Replacement Cost: Policies under the FAIR Plan often cover the actual cash value of the property, which accounts for depreciation, rather than the full replacement cost. Homeowners must cover the difference out of pocket, which can be tens or hundreds of thousands of dollars. Even when a home is rebuilt, this approach fails to make homeowners whole, as they often cannot replace belongings or upgrade to meet modern building codes.

- Lack of Additional Living Expenses (ALE): Unlike standard homeowner’s insurance policies, the FAIR Plan does not cover temporary housing or other living expenses incurred while rebuilding. Victims of the Eaton and Altadena fires who lost their homes now face extended displacement and significant financial burdens, as these costs fall squarely on their shoulders.

- Underestimation of Property Values: The FAIR Plan relies on property assessments that can be outdated or inaccurately reflect the market value of homes in high-value areas like Malibu and the Palisades, leaving homeowners severely underinsured.

- Limited Funding Pool: The FAIR Plan’s resources are finite. It is not a state-funded program but rather a pool funded by all property insurance companies operating in California. With the surge in claims following the January fires, the strain on the FAIR Plan’s resources is evident.

FAIR Plan in the Context of the January 2025 Fires

Palisades Fire

In the Palisades fire, where property values are high, the FAIR Plan’s limitations have been particularly glaring. Homeowners who lost properties have reported that their coverage was insufficient to rebuild, especially given rising construction costs and inflation. Without ALE coverage, many families have struggled to secure temporary housing, which is scarce after a widespread disaster.

Altadena Fire

The Altadena fire devastated a diverse community, leaving many residents relying on the FAIR Plan due to the area’s high fire risk. The FAIR Plan’s policy limits have left these homeowners unable to rebuild or replace their homes, amplifying financial distress. In such cases, seeking legal assistance from our Altadena fire attorney or our fire insurance claim lawyer can help residents navigate these challenges and advocate for adequate compensation. The Altadena fire devastated a diverse community, leaving many residents relying on the FAIR Plan due to the area’s high fire risk. The FAIR Plan’s policy limits have left these homeowners unable to rebuild or replace their homes, amplifying financial distress.

Eaton Fire

Although some properties in the Eaton fire were spared from direct fire damage, smoke and ash caused extensive harm. The FAIR Plan’s strict criteria for fire damage coverage have left many claims denied or underpaid, forcing homeowners to navigate a bureaucratic and financially draining process. In these situations, consulting with our Eaton fire attorney or fire damage insurance claim attorney can help homeowners understand their rights and fight for the compensation they deserve. Although some properties in the Eaton area were spared from direct fire damage, smoke and ash caused extensive harm. The FAIR Plan’s strict criteria for fire damage coverage have left many claims denied or underpaid, forcing homeowners to navigate a bureaucratic and financially draining process.

Malibu Fire

The Malibu fire, with its history of wildfires and high property values, has seen its residents particularly hard-hit. The high cost of construction and the complexity of rebuilding in a coastal zone have made the FAIR Plan’s payouts inadequate. Additionally, the lack of ALE coverage has forced families into precarious financial situations as they navigate temporary housing options. Engaging with our Los Angeles wildfire attorney or our fire damage insurance claim attorney can provide critical support to ensure fair treatment during the claims process. Malibu, with its history of wildfires and high property values, has seen its residents particularly hard-hit. The high cost of construction and the complexity of rebuilding in a coastal zone have made the FAIR Plan’s payouts inadequate. Additionally, the lack of ALE coverage has forced families into precarious financial situations as they navigate temporary housing options.

Topanga Fire

The Topanga fire underscored the disparity between FAIR Plan payouts and actual rebuilding costs. Homeowners in this wooded area face the added expense of rebuilding to meet modern fire-resistant building codes, costs that the FAIR Plan does not cover.

Hurst Fire

The Hurst fire, which has already endured previous wildfire seasons, the FAIR Plan’s restrictions have compounded challenges for homeowners. Delayed claims processing and insufficient payouts have hindered rebuilding efforts, leaving many residents in limbo.

Concerns About FAIR Plan’s To Pay All Homeowners’ Losses

As the frequency and intensity of wildfires increase, more Californians are turning to the FAIR Plan. Its total exposure has surged to $458 billion, reflecting a 61.3% increase since September 2023. This growing demand raises serious questions about the plan’s financial sustainability. With estimated damages from the January 2025 fires far exceeding the FAIR Plan’s capacity, homeowners face significant delays in claims processing and payouts.

The Emotional Toll on Homeowners

The January 2025 fires have left a deep emotional scar on affected communities. Many homeowners, believing they were adequately insured, have been forced to rely on savings, take out loans, or turn to family and friends to make up for the shortfall. Even for those who can rebuild their homes, the financial and emotional toll of losing cherished possessions, navigating the claims process, and covering gaps in coverage often leaves them far from whole. Seeking support from experienced legal professionals, such as our fire insurance lawyer or our wildfire insurance attorney, can be critical in navigating this difficult period and ensuring fair treatment by insurers.

The January 2025 fires have left a deep emotional scar on affected communities. The FAIR Plan’s inadequacies add insult to injury, exacerbating the stress and uncertainty of losing a home. Many homeowners, believing they were adequately insured, have been forced to rely on savings, take out loans, or turn to family and friends to make up for the shortfall. Even for those who can rebuild their homes, the financial and emotional toll of losing cherished possessions, navigating the claims process, and covering gaps in coverage often leaves them far from whole.

Calls for Reform

The FAIR Plan’s limitations have sparked widespread calls for reform. Key areas of focus include:

- Increased Coverage Limits: Raising policy limits to reflect the true cost of rebuilding in high-value areas like Malibu and the Palisades.

- Comprehensive Coverage Options: Expanding the FAIR Plan to include ALE, liability, and other standard policy features.

- Transparent Valuation Processes: Ensuring property values are accurately assessed to prevent underinsurance.

- State Support: Allocating state funds to bolster the FAIR Plan’s resources and ensure adequate payouts during large-scale disasters.

- Streamlined Claims Processing: Reducing delays to provide homeowners with the financial support they need more quickly.

For homeowners who feel overwhelmed, our California fire attorney or our LA fire lawyer can provide legal guidance to navigate the claims process and advocate for fair compensation. Whether it’s assistance from our SoCal fire attorney or representation by our fire damage insurance claim attorney, these experts are instrumental in securing better outcomes for fire victims.

The FAIR Plan’s limitations have sparked widespread calls for reform. Key areas of focus include:

- Increased Coverage Limits: Raising policy limits to reflect the true cost of rebuilding in high-value areas like Malibu and the Palisades.

- Comprehensive Coverage Options: Expanding the FAIR Plan to include ALE, liability, and other standard policy features.

- Transparent Valuation Processes: Ensuring property values are accurately assessed to prevent underinsurance.

- State Support: Allocating state funds to bolster the FAIR Plan’s resources and ensure adequate payouts during large-scale disasters.

- Streamlined Claims Processing: Reducing delays to provide homeowners with the financial support they need more quickly.

For homeowners who feel overwhelmed, our California fire attorney or our LA fire lawyer can provide legal guidance to navigate the claims process and advocate for fair compensation.

The FAIR Plan’s limitations have sparked widespread calls for reform. Key areas of focus include:

- Increased Coverage Limits: Raising policy limits to reflect the true cost of rebuilding in high-value areas like Malibu and the Palisades.

- Comprehensive Coverage Options: Expanding the FAIR Plan to include ALE, liability, and other standard policy features.

- Transparent Valuation Processes: Ensuring property values are accurately assessed to prevent underinsurance.

- State Support: Allocating state funds to bolster the FAIR Plan’s resources and ensure adequate payouts during large-scale disasters.

- Streamlined Claims Processing: Reducing delays to provide homeowners with the financial support they need more quickly.

Conclusion

The January 2025 wildfires have exposed critical shortcomings in the California FAIR Plan’s ability to protect homeowners in high-risk areas. With estimated damages far exceeding the plan’s coverage limits and financial capacity, affected residents face significant challenges in rebuilding their lives and properties. Comprehensive reforms are urgently needed to ensure the FAIR Plan can fulfill its promise of safeguarding Californians in their most vulnerable moments. Until such changes are implemented, homeowners in fire-prone regions remain at risk of being left financially and emotionally devastated.